Check your estimated monthly payments, PMI thresholds, and principal loan adjustments.

How to Use the Mortgage Finder & Calculator

Set Purchase Price

Enter the total market value or target purchase budget for the residential property.

Adjust Down Payment

Input your available upfront cash to instantly see your loan-to-value (LTV) percentage balance.

Select Loan Program

Pick your preferred amortization timeline and market interest rate from the dropdown menu.

Run the Assessment

Click “Calculate My Payment” to generate a detailed monthly breakdown of your principal and interest costs.

Why Trust Our Mortgage Calculator?

We provide transparent financial forecasting designed for the modern American real estate landscape.

Certified Amortization Engine

Calculations use traditional banking algorithms, giving you standard baseline expectations for both fixed principal and structural interest margins.

Zero Tracking Policy

We do not store your loan values, down payments, or asset choices. Your residential planning session stays completely private on your machine.

Frequently Asked Questions

What factors determine my final monthly mortgage payment?

Your base payment is determined by the total loan size, down payment ratio, interest rate, and term length. Real-world structural setups will also factor in local property taxes, homeowners insurance premiums, and private mortgage insurance (PMI) if your down payment is under 20%.

Is a 15-year fixed loan better than a 30-year fixed loan program?

A 15-year fixed loan accelerates your equity building and saves substantial interest over the lifespan of the loan, but requires higher monthly installments. A 30-year option maximizes your near-term cash flow flexibility by lowering the individual monthly commitment.

How does down payment scale change my mortgage interest burden?

Putting more cash down reduces your starting principal balance. Because mortgage interest calculations compound based on your remaining debt profile, a larger initial down payment lowers total lifecycle interest accumulation.

Disclaimer: This digital tool provides structural approximations for educational purposes only. Calculated metrics do not represent accurate loan packaging terms, underwriting commitments, or locked financial interest quotes. Closing adjustments, secondary market shifts, insurance options, and credit profile variations will alter real-world configurations. Consult a certified financial representative or certified US lending broker before executing real estate contracts.

Are you accidentally donating thousands of dollars to the IRS? Millions of US homeowners cross the standard deduction threshold every year but completely miss out on their structural wealth shield. If you do not lock in your strategic filing parameters before the hard December 31 statutory midnight deadline, your unclaimed write-offs disappear forever. Read below to claim your asset defense.

The Homeowner’s Shield: Mastering the Mortgage Interest Tax Deduction to Erase Federal Liability

Stop renting your capital. Transform your standard housing debt into a powerful federal wealth-shield instantly.

For the modern digital entrepreneur and high-earning asset builder, progressive federal taxation acts as a silent cash flow drain. However, the internal revenue code holds a massive structural loophole specifically engineered for real estate financing. By systematically tracking your regular monthly debt repayments and pivoting from a flat standard deduction to an aggressive itemized strategy, you can legally isolate your property costs to build an impenetrable shield around your sovereign revenue.

Every single month, professional high-earners and scaling digital founders watch their hard-earned liquid wealth evaporate into the progressive federal tax drag. You work around the clock to scale your revenue, yet the moment your income climbs into a higher marginal bracket, the IRS automatically penalizes your growth by capturing massive percentages of your cash flow. Renting a premium residential property or mismanaging your real estate financing structure feels like a double financial loss—you are essentially writing a massive check to landlords or the government without building an active asset protection shield around your core business ecosystem.

It is incredibly frustrating to build sovereign revenue assets only to see thousands of dollars slip through your fingers due to a reactive tax approach. Many ambitious W-2 professionals and entrepreneurs feel completely trapped when executing standard, flat-rate filings because they assume tax planning is reserved solely for institutional corporations. Leaving hard-earned capital entirely exposed to aggressive deductions leaves you stuck in a cycle of overpaying on your true liability, especially when your primary residential mortgage debt could easily be serving as your absolute primary wealth-shield.

The ultimate strategy to crash your federal liability lies in systematically deploying the legal mechanics of the mortgage interest tax deduction. This comprehensive technical guide provides an elite architectural blueprint to help you transition smoothly from standard deduction limitations to aggressive Schedule A itemization. By accurately mapping your qualified acquisition indebtedness limits, aligning your cash flow needs, and utilizing the custom computational tools below, you will completely eliminate financial guesswork, optimize your blended average effective rate, and force your debt to build long-term wealth velocity.

Guide Architecture

The Financial Friction: Progressive Tax Drag vs. Homeownership Costs

For the high-earning asset builder, independent digital contractor, and modern founder, progressive federal taxation acts as a relentless, compounding cash flow drain. The foundational mechanics of the U.S. tax framework are inherently designed to penalize aggressive revenue growth; as your earnings scale across marginal brackets—shifting from 22% and 24% up into the 32%, 35%, and 37% tiers—the absolute percentage of liquid capital captured by the government expands exponentially. This structural phenomenon is known as progressive tax drag, and without a deliberate intervention layer, it systematically dilutes your operational wealth velocity.

Many ambitious individuals view residential real estate simply as a lifestyle milestone or a rigid debt obligation. However, continuing to rent a premium primary residence or mismanaging your property financing structure means writing a 100% unrecoverable check month after month. To build an impenetrable asset shield, you must transform your primary housing liabilities into active tax-mitigation engines. Understanding and implementing the legal mechanics of the mortgage interest tax deduction is not merely a filing preference—it is a critical wealth preservation mandate required to alter your true, blended effective tax rate.

To verify how these progressive thresholds directly penalize unshielded income streams, you can audit the official statutory parameters directly via the Internal Revenue Service (IRS) Tax Brackets Guidelines. Reviewing these primary governmental matrices reveals exactly why leaving your revenue exposed to standard formulas leaves thousands of dollars on the table.

Strategy 1: Transitioning from Flat Standard Thresholds to Schedule A Itemization

The initial filter in your wealth-protection strategy requires winning a mathematical battle: the standard deduction versus itemized deductions. The vast majority of standard filers lazily opt for the flat standard deduction because it requires zero tracking friction. However, for a high-earner who has recently secured residential financing, accepting this flat threshold is a massive strategic mistake that artificially inflates your adjusted gross income (AGI).

To legally bypass the standard limitations, your total qualified personal expenditures must exceed the government’s baseline ceiling. By actively consolidating your property interest payments with your state and local tax allocations, you can easily clear the flat standard barrier and unlock uncapped federal liability reductions on Schedule A.

⚡ Strategic Action Plan

- Consolidate Your Data Points: Aggregate your annual Form 1098 (Mortgage Interest Statement) directly alongside your localized property tax receipts.

- Execute the Core Math: Total your exact property interest expenses, add your eligible state and local taxes (SALT caps limit this to a maximum of $10,000), and add any verified charitable contributions.

- Deploy Schedule A: If this combined total outpaces the fixed standard deduction threshold for your filing status, bypass the standard option entirely and itemize your profile to capture every single dollar of structural savings.

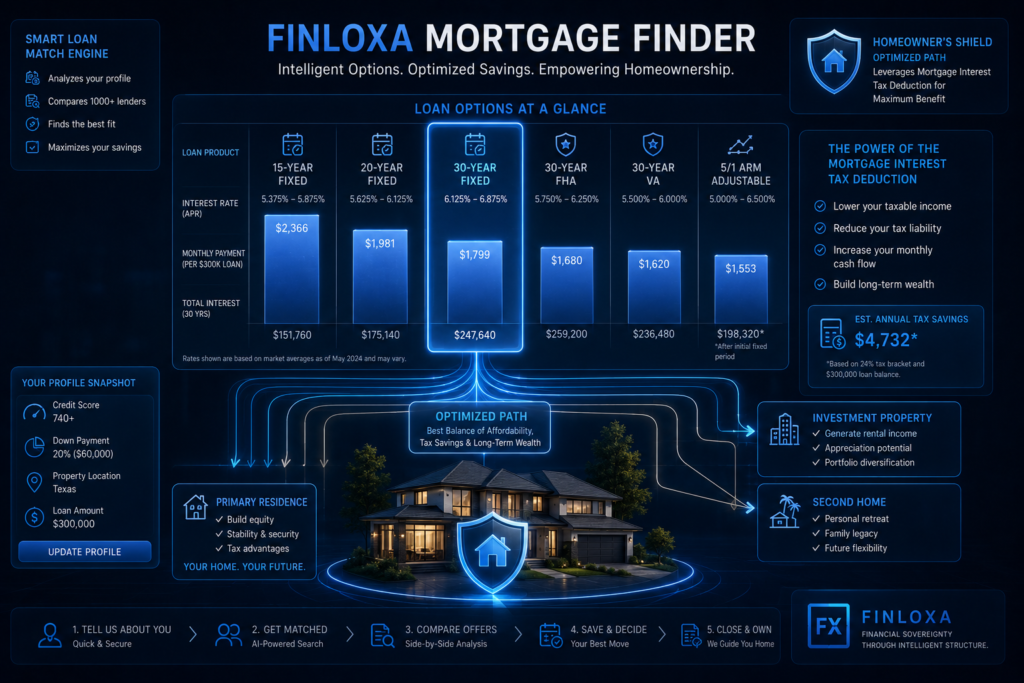

Strategy 2: Calibrating the $750,000 Acquisition Indebtedness Shield

Once you commit to an itemized filing framework, you must align your debt architecture with strict statutory limits. Under current internal revenue codes, the mortgage interest tax deduction is restricted to a specific debt ceiling known as qualified acquisition indebtedness. For any primary or secondary residential mortgage secured after December 14, 2017, homeowners can deduct the interest paid on a maximum of $750,000 of total loan principal (or $375,000 if married filing separately).

Any debt borrowed beyond this hard $750,000 threshold is classified as non-qualified, meaning the interest tied to that excess capital provides absolutely zero structural tax benefit. Furthermore, the capital must have been deployed strictly to buy, build, or substantially improve the qualified residence that secures the underlying loan.

If your overall property financing exceeds the statutory $750,000 principal boundary, your tax professional must apply a specific fractional reduction formula to isolate your deductible interest. To maximize your front-loaded cash flow value, consider executing a targeted principal buy-down or purchasing discount points during your initial financing or refinancing phases. This approach allows you to convert standard, long-term financing interest into immediate, front-loaded pre-tax deductions that lower your taxable income.

Strategy 3: Deploying Dynamic Interest Amortization to Protect Revenue

To truly understand why mastering this deduction is essential to your long-term wealth velocity, you must analyze the mechanics of a standard fixed-rate mortgage amortization schedule. During the initial five to ten years of a residential loan, your monthly repayments are heavily front-loaded with interest rather than principal reduction. While this reality is often viewed as a major downside of long-term financing, it actually creates a powerful, highly concentrated federal tax shield during your peak income-generating years. Because the interest component of your payment is at its absolute peak during the infancy of the loan, your itemized deduction capacity is naturally maximized precisely when you need to offset aggressive marginal brackets.

Tax Optimization Matrix

| Financing Tier & Indebtedness Type | IRS Principal Limits | Immediate Cash Flow Impact | Structural Advantage on Schedule A |

|---|---|---|---|

| Qualified Acquisition Debt | Up to $750,000 | Maximum Impact; instantly offsets highest marginal brackets. | 100% of internal interest expense is fully deductible against federal liability. |

| Excess Non-Qualified Debt | Above $750,000 | Zero Impact; interest on excess capital is completely exposed. | Interest must be fractionally prorated and is excluded from tax-shield value. |

| Home Equity Loans (HELOCs) | Combined up to $750,000 | Variable; depends strictly on verified capital deployment. | Only deductible if capital was used exclusively to build or substantially renovate the property. |

[Insert Image/Chart 1: The Amortization Tax Shield Graph right here. This visual asset should contrast a standard declining interest curve against your climbing marginal tax brackets, illustrating exactly how front-loaded interest payments act as an aggressive cash shield during the first decade of your loan.]

For an absolute deep dive into how these property financing rules overlap with broader capital asset frameworks and verified investment parameters, cross-reference your calculations directly with the official U.S. Department of the Treasury Data Portals.

Strategy 4: The Advanced Entrepreneurial Home Office Overlay

For independent digital creators, corporate entities, and online founders, the optimization playbook goes even deeper by blending personal real estate deductions with business expense tracking. If you operate a verified digital enterprise from your primary residence, you can strategically combine your mortgage interest tax deduction framework with home office write-offs. By calculating the exact square footage of your dedicated, exclusive operational workspace relative to the total square footage of the property, you can allocate a proportional slice of your residential costs directly as an above-the-line business expense.

This strategic overlay allows you to shift a portion of your housing expenses out of Schedule A itemization and directly into your pass-through entity framework (such as an LLC or S-Corporation). The immense value here is dual-layered: the allocated portion not only reduces your overall federal income tax base, but it also lowers your self-employment tax obligations. By actively running your year-to-date income figures through precision software, you can isolate the ideal mathematical equilibrium point between personal itemized structures and corporate deductions. This ensures you eliminate the stress of guesswork and maintain total, audit-proof control over your wealth.

The Execution Pipeline: How to Claim Your Mortgage Interest Shield

Transforming your housing liabilities into an audit-proof tax mitigation engine requires executing a precise chronological playbook. You cannot afford to guess when dealing with internal revenue regulations; a single filing misstep can trigger structural non-compliance or cause you to unintentionally forfeit thousands of dollars in legitimate deductions. Follow this multi-phase framework to systematically lower your adjusted gross income (AGI) and optimize your sovereign wealth velocity.

Step 1 Preparation (Data Consolidation and Mathematical Validation)

The foundation of any successful tax shielding maneuver relies strictly on structural verification before your filing date. Before you can completely abandon the flat standard deduction, you must aggregate your physical and digital financial footprints to prove your total expenditures outpace the government’s baseline threshold. This phase acts as your primary optimization filter.

Isolate Your Form 1098: Secure the official Form 1098 (Mortgage Interest Statement) directly from your primary institutional lending portal as soon as the fiscal period closes. This statutory form outlines your exact calendar-year interest contributions.

Audit Your Closing Disclosures: If you purchased or refinanced your residential property during the current tax year, carefully review your settlement statements to calculate deductible loan origination points.

Track Localized Property Levies: Consolidate your localized real estate property tax receipts, ensuring you calculate the exact state and local allocations tied directly to your underlying asset base.

Step 2 Implementation (Mapping Deductions to Schedule A)

Once your baseline data points are validated, you must structurally execute the math to shift your profile from a flat deduction to aggressive itemization. This phase is where your financial variables interact directly with the IRS code matrices. You will map your individual numbers directly onto Schedule A (Form 1040) to construct your personal tax shield.

Execute the Absolute Floor Test: Compare your cumulative property interest, eligible state and local taxes (SALT capped up to $10,000), and charitable metrics against the fixed flat standard deduction threshold matching your specific filing status.

Apply Fractional Prorating Formulas: If your primary or secondary loan principal outpaces the strict $750,000 qualified acquisition indebtedness limit, calculate your exact deductible percentage by dividing $750,000 by your true balance.

Transfer Metrics to Form 1040: Enter your verified interest variables directly onto Line 8a or Line 8b of Schedule A, embedding the data safely within your broader progressive federal return structure.

Step 3 Review and Finalize (Audit Defense and Systems Calibration)

Securing the Value Layer Through Strict Technical VerificationThe final mile of your implementation strategy requires building a defensive boundary around your deductions to completely eliminate audit vulnerability. Never hit the final submission button without cross-checking your variables against structural red flags. You must preserve comprehensive documentation to defend your deductions in the event of an institutional review.

Verify Capital Deployment Trails: Ensure any interest claimed on secondary Home Equity Loans of Credit (HELOCs) is backed by concrete digital or physical invoices proving the capital was deployed exclusively to build, buy, or substantially improve that exact residence.

Sync Enterprise and Personal Overlaps: If you are deploying an advanced entrepreneurial home office overlay, strictly separate the percentage of interest claimed on your corporate pass-through schedules from the personal deductions remaining on Schedule A.

Archiving Your Defense Ledger: Store your digital Form 1098 assets, escrow ledgers, and property tax receipts in an independent secure vault for a minimum of three to seven years to maintain a perfect, unassailable paper trail.

Phase Execution Reference Matrix

| Execution Phase | Core Objective | Key Statutory Document | Critical Compliance Parameter |

|---|---|---|---|

| Step 1: Preparation | Data collection and baseline verification. | Form 1098 / Settlement Statements | Confirming interest calculations are cleanly separated from principal pay-downs. |

| Step 2: Implementation | Active data mapping onto federal schedules. | Schedule A (Form 1040) | Applying fractional proration equations if total mortgage debt outpaces $750,000. |

| Step 3: Review | Audit defense building and final filing safety. | Internal Expense Ledger | Maintaining clean, independent spatial tracking for home office overlaps. |

Weighing Your Options: Standard Blindness vs. Itemized Wealth Shields

Making a definitive filing choice should never be based on guesswork; it requires auditing the exact mathematical variance between standard corporate limits and structural real estate deductions. If your personal annual housing debt costs are sitting safely below the government’s flat threshold, rushing into itemization simply adds unnecessary tracking friction to your workflow.

However, the moment your qualified acquisition indebtedness, localized property levies, and state allocations outpace that flat ceiling, choosing the standard route forces you to pay a massive, unnecessary penalty directly to the IRS. For modern founders and high-income professionals scaling assets across progressive tax brackets, making the deliberate transition to an itemized shield is the ultimate mechanism to instantly free up liquid capital, optimize cash flow velocity, and maximize year-over-year asset protection.

Strategic Filing Matrix: A Comparative Evaluation

| Financial Variable & Performance Metrics | The Flat Standard Route (Passive Filing) | The Strategic Itemized Shield (Schedule A) | The Direct Bottom-Line Impact |

|---|---|---|---|

| Adjustment to Adjusted Gross Income (AGI) | Restricted strictly to the baseline flat-rate threshold determined by your filing status. | Directly scales based on true property debt interest up to the hard $750,000 principal boundary. | Itemized Wins: Instantly compresses your taxable base during high-earning infancy years of amortization. |

| Tracking Friction & Data Management | Zero Management; requires no digital receipt vaulting or Form 1098 aggregation. | Requires systematic tracking of mortgage interest statements, closing documents, and SALT metrics. | Standard Wins on Speed; Itemized wins massively on long-term net capital retention. |

| State and Local Tax (SALT) Integration | Completely unavailable; local real estate allocations provide zero financial advantages. | Allows smooth integration of local property and income levies up to a strict $10,000 statutory cap. | Itemized Wins: Unlocks combined deduction values that easily destroy the flat standard threshold floor. |

| Enterprise Space Overlays (Home Office) | Limited to standard flat-rate equations unless utilizing complex independent corporate schedules. | Seamlessly pairs with advanced proportional spatial tracking to reduce self-employment tax drag. | Itemized Wins: Transforms ordinary residential liabilities into multi-layered corporate write-offs. |

If your combined calendar-year metrics—specifically your verified Form 1098 interest totals added directly to your $10,000 maximum eligible SALT allocations—clear the baseline standard deduction threshold for your specific filing status, you must execute an itemized Schedule A return immediately. Remaining passive under a standard filing model means volunteering your hard-earned wealth back to the federal government. Take total control of your numbers, deploy your asset shield, and secure your financial sovereignty today.

Frequently Asked Questions: Mortgage Interest Tax Optimization

Q: Can I claim the mortgage interest tax deduction if I take the standard deduction?

A: No. The federal mortgage interest tax deduction is strictly an itemized deduction calculated on Schedule A (Form 1040). If you opt for the flat standard deduction, you completely forfeit the right to write off any personal real estate interest expenses or localized property levies for that fiscal period.

Q: What is the maximum mortgage limit for interest tax deductions?

A: For residential properties acquired or financed after December 14, 2017, you can deduct interest paid on a maximum hard ceiling of $750,000 of qualified acquisition indebtedness (or $375,000 if married filing separately). Loans grandfathered in prior to that date retain a legacy limit of $1,000,000.

Q: Is interest on a Home Equity Line of Credit (HELOC) tax deductible?

A: Yes, but with strict IRS conditions. HELOC interest is only deductible if the underlying capital was deployed exclusively to buy, build, or substantially improve the qualified secondary or primary residence securing the loan. If used to consolidate personal credit card debt or buy consumer vehicles, the interest is completely non-deductible.

Q: How do I find out the exact amount of mortgage interest I paid this year?

A: Your institutional lending bank or servicer is legally required to send you a Form 1098 (Mortgage Interest Statement) by January 31 following the close of the tax year. This official document reflects your exact interest variables, prepaid points, and localized escrow real estate taxes paid.

Q: Can digital founders combine home office write-offs with mortgage interest deductions?

A: Yes. If you qualify for the home office deduction, a proportional slice of your mortgage interest is allocated directly onto your business entity schedules (reducing self-employment drag), while the remaining personal balance is funneled directly into your personal Schedule A itemized layout.

Securing the Shield: Your Next Steps to Sovereign Wealth

Navigating the complex layers of federal tax mitigation requires a shift from passive compliance to active wealth calibration. As we have mapped out across this architectural layout, executing a transition from standard boundaries to an aggressive, well-documented Schedule A itemized strategy is the single most effective move to stop progressive tax drag from eroding your liquid cash flow. Protecting your revenue is not just about filing clean forms—it is about making your real estate liabilities work directly for your long-term balance sheet.

With the clear data metrics from your **Form 1098**, calculated **SALT allocations**, and advanced structural frameworks like the **home office enterprise overlay**, you hold the complete blueprint required to claim your statutory asset shield. You have the knowledge and the framework; do not leave your hardest-earned capital entirely exposed to default IRS parameters.

Ready to Eliminate the Guesswork?

Take immediate charge of your numbers today. Scroll back to the top of this guide to run your parameters through our live Interactive Mortgage & Tax Estimator Tool, accurately isolate your exact acquisition boundaries, and lock down your financial footprint before the next statutory deadline.

Calculate Your Savings Now 📊About the Founder

Digital Entrepreneur | Financial Systems Architect

As the architect behind Finloxa.com, I engineer high-velocity asset and tax optimization systems for global creators and modern founders. My focus is breaking down advanced IRS property codes, mortgage debt parameters, and strategic itemization metrics into clean, data-driven automation pipelines.

Optimize Your Residential Real Estate Finance Legally

Accurately evaluating your mortgage interest tax deduction options is the ultimate step to protect your wealth from aggressive erosion. Take total control of your cash flow layout using my custom computational engines and advanced shielding frameworks.

Empowering entrepreneurs with the “The Filter, The Engine, and The Value Layer” tax optimization methodology.